Summary

- Its reserve status and most recent capital inflows have kept the dollar very strong

- However, Trump’s plans for Ukraine suggest an unloved Euro is cheap

- That is an understatement if increasing talk of a Mar-a-Lago Accord has legs

- History and our models suggest the dollar is ripe for a 30-40% correction

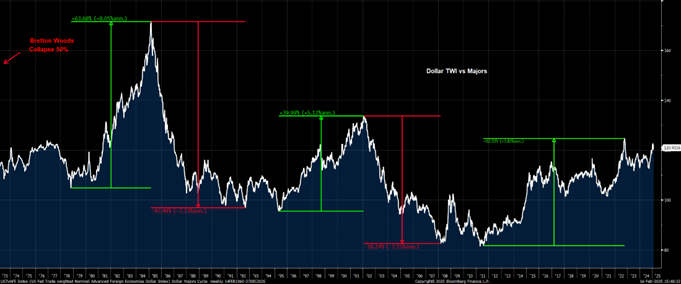

It’s the middle of February again, which means the dollar is on our radar. That’s because since the end of Bretton Woods in the early 1970s, over 80% of the time, the dollar has made its highs or lows for the year vs European FX (in this case, the Deutschemark) in Q1.

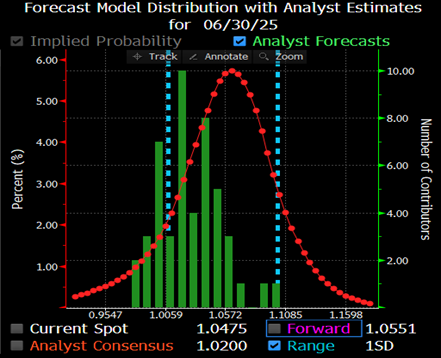

So the obvious question is, are we looking at a high or a low? As we rolled into January, between nascent signs of surging US data and talk of tariffs, 2025 was shaping up to be a strong dollar year. Indeed, as you can see in the graph below, the consensus from the FX analysts is that by the end of June, EURUSD will be 1.0200. Yet, in the last two weeks, we have seen a reversal in this trend. Perhaps it is simply position adjustment in a market late getting into the strong USD trade and now over its risk skis? Don’t forget that the relative sentiment between the US and Europe was extreme at the start of the year (“Europe: Peak Pessimism Creates Opportunity” 6th Feb). If that is the case, then after a correction, the dollar’s dominance will reassert itself, and any current bearish talk is simply narrative fitting.

However, our spider senses are tingling with rumours of various policies being ruminated on by the Trump Administration. At this stage, there is very little concrete information and a lot of conjecture. But if the rumours are correct, we could be looking at a series of steps that result in not just a garden-variety dollar top but the most significant market event in the last forty years.

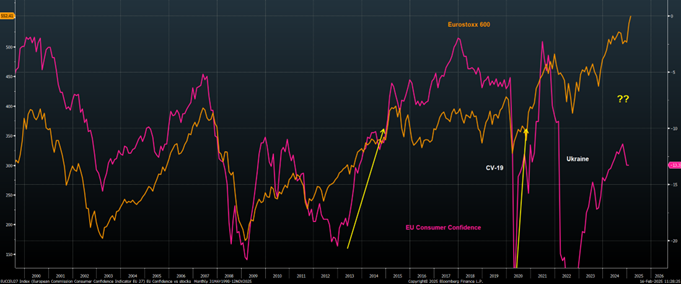

The most tangible and imminent step on this path to dollar weakness would be a deal on the Ukraine. That’s because, while Europe’s globalist elite are still aghast at their exclusion from the proposed US/Russia peace summit in Saudi and reeling from JD Vance’s broadside at the Munich Security Conference, the reality is that peace would be great news for the European economy. First, if the deal involves Russian gas flowing back into Europe, the effect on the German economy would be transformative, and some very cheap energy-sensitive stocks could really benefit (Bayer, BASF, ThyssenKrupp, Salzgitter and even the car companies). P.S. As discussed on the 6th, the odds of a Nord Stream deal will rise materially if the AfD forms part of a new German government. Furthermore, given that the invasion crushed European consumer confidence, any peace deal could be a real boost, especially if stocks were to rise further. In this scenario, it isn’t hard to imagine that some of the very aggressive cuts currently priced into the Euribor curve get removed to the benefit of the Euro.

That brings us to any peace deal’s second and potentially most significant impact. As we all observed, there was a material shift in global capital flow immediately following the invasion, as European investors sought the relative safety of US markets. At the time, this money was easily absorbed by the funding demands of the US current account and budget deficits, which are an integral part of the current US reflexive cycle. The downside of all this inflow is that the US has become the piggybank for global savings, and Europe, in particular, has seen its assets in the US grow significantly. Therefore, if we get a peace deal, the cost of rebuilding Ukraine, which the World Bank estimates at just under $500bln, will have to be funded by the Europeans withdrawing their savings from US markets. Add increased defence spending to appease the Trump Administration and avoid swingeing tariffs, and the funding demands could be considerable.

Thus far, we have examined possible reasons EURUSD could move higher. But we will now focus on why we need to consider the possibility that this is just part of the story, which could mark a major dollar top.

In 2019, we wrote a series of pieces outlining how the likes of the Gilet Jaune, UKIP and Trump were emblematic of a rising tide of popularism that felt that the current economic orthodoxy of neo-liberalism with its unbridged globalisation was failing them (“RIP Corporate Capitalism” 7th Feb 2019). When we wrote the pieces, these forces had unquestionably widened the “Overton Window” (the window of permissible political discourse). However, these movements were in their infancy, and while there was plenty of anger, there was little in the way of detailed policy objectives.

Fast forward six years, and the desire for change is increasingly palpable, but most importantly, these parties have had time to refine their policies. This is why, immediately after the US election, we warned that the market’s assumption that Trump 2.0 would be a mirror image of 1.0 was too simplistic. Investors forgot that while the President is sensitive to stocks, his target audience wasn’t Wall Street but Main Street, i.e., the workers of America. This is a constituency that rightly feels that corporate America’s endless offshoring has sold them out, a process which, at the same time, undermines the US’s hegemonic standing and, from our understanding, means that some senior members of the Administration believe we are in a make-or-break moment regarding the sustainability of the government debt. Hence, something dramatic is required, which is why we suggested that by late January, the market would start to wake up to the reality of facing “material changes to the current status quo in markets and global trade” (“The Three Stages of a Trump Presidency” 8th Nov 2024). At the time, the main policies on the radar were tariffs and immigration control. But fast forward a few months, and we are getting glimpses of a far more ambitious plan.

At the end of last year, Hudson Bay Capital issued a research piece called “A Users Guide to Restructuring the Global Trading System”. At the time, it got limited attention because while Stephen Miran, its author, had written a fantastic piece of research dissecting Yellen’s manipulation of the Treasury market, he and the firm were relatively unknown. However, since Stephen has been nominated as Chair of the Council of Economic Advisors, suddenly, we hear talk of sovereign wealth funds, monetising US assets and a possible Mar-a-Lago Accord.

Essentially, in his work, Stephen outlines how the US has reached Triffin’s Dilemma, where the benefits derived from maintaining the reserve currency no longer offset the domestic costs. However, rather than go quietly, letting Pax Americana and the dollar slide into oblivion, he has a plan, which boils down to several key elements:

- Active intervention in the FX markets to mimic and offset some countries’ mercantilist manipulation to keep their currencies artificially cheap. (P.S. We assume the foreign assets would be placed in the new sovereign wealth fund).

- Disincentivise the accumulation of dollar reserves by charging foreign central banks or sovereign wealth funds fees for holding Treasuries.

- Force other countries to pay to be part of the US’s security umbrella by forcing them to swap their existing Treasury holdings for hundred-year bonds with no yield (P.S. these aren’t zeros bought at a discount).

- Levy tariffs on countries that run persistent trade surpluses, don’t play by the rules or even refuse to accept the debt swap.

- Use the Fed to actively sterilise any monetary implication of FX intervention and stabilise any excess volatility in the Treasury market as the plan is implemented.

- Pursue bilateral/multilateral trade deals and strategic partnerships to undermine adversaries and improve ties to allies.

- Aggressively pursue deregulation and energy production to offset any inflation.

WOW! We expected a material change to the current status quo in markets and global trade. But even we didn’t think they would go this far because, frankly, the fallout could be disastrous when we look at the list of proposals. (We will look at broad consequences in a follow-up piece). Instead, today, we are just interested in the dollar, and if Mr Miran gets his way, there is no question that it will put the skids under the buck! Indeed, while the objective is to preserve the dollar’s reserve standing, even the paper acknowledges the risk that these steps could encourage rivals such as the RMB. The good news is that while the ideas are being considered, nothing is concrete yet, and even if they come to fruition, implementation will be gradual. That said, for the first time in many years, we have a possible roadmap that could dictate the dollar’s trajectory for the next decade.

That raises the question of just how far the dollar could fall. Before we start looking at particular levels, we want to remind you that we are not talking about the demise of the dollar as the global reserve currency, just the possibility of a 30-40% decline, which is typical of a normal cycle.

Interestingly, when we look at individual currency pairs, they also suggest that declines of similar magnitudes are possible. However, there is something even more intriguing. Time and time again, we see relationships that have worked for decades suddenly break down, starting around 2020/21. As we have discussed, some of this is related to the process whereby money is recycled back into the US to fund a current account deficit that has exploded over the last 5 years from $400bln a year to over $1.2tln. Essentially, we have a massive vendor financing cycle.

Starting with EURUSD, we have shown you how, despite successive waves of central bank intervention, the currency pair always returned to the anchor of our trade model. That was until 2021, when the model shot higher, suggesting that the current fair value for EURUSD is closer to 1.5000.

Switching to AUDUSD, our terms of trade model suggests that, absent the recycling of trade flows, the correct value of the currency pair is 0.9000.

Meanwhile, a similar model for USDCAD yields a level of 1.1800.

Finally, to Korea, which, with its massive trade surplus and US troops on the ground, is a perfect candidate to “pay their fair share”, and here, a “fair value” target is 960.00. P.S. Remember given the level of speculation in US stocks by Korean investors, the currency is more vulnerable than most to any decline in the major US equity indexes.

We don’t have models for every currency pair, but you get the general picture. Indeed, to reinforce the dollar’s spectacular performance, below is a chart in which we have normalised its percentage gains against the major tradable currencies since it started to rally in 2011. Effectively, it’s a “rich/cheap” type of analysis and suggests that if you are a dollar bear, you should be watching NOK, Yen, MXN, and our favourite SEK.