Summary

- From Trump to Gilet Jaune, events suggest we are approaching a political regime shift

- We believe it is likely to pressure the reforms of the 1980s Reagan-Thatcher revolution

- Popularism that reduces free-market liberalism will create a tougher business environment

- On a macro basis, expect mounting pressure on profits and multiples.

“Turning and turning in the widening gyre

The falcon cannot hear the falconer;

Things fall apart; the centre cannot hold;

Mere anarchy is loosed upon the world”

-WB Yeats

From time to time, we like to turn our minds to big-picture themes which don’t necessarily have an immediate trading application. For example, over the summer we discussed a structural shift in the US/China relationship (“When Love Breaks Down” 3rd Sept 2018). As it turned out that piece was prescient and timely. But whether that’s the case or not is immaterial because in a business like ours it’s easy to get lost in the weeds and lose sight of the big picture.

Today, we focus on the rising tide of populism. Where has it come from, does it have legs, and if so, what are the macroeconomic implications? In particular, is it a coincidence that it is emerging after a thirty plus year run of deregulation and unbridled laissez-faire economic policy? In tackling these questions, this piece will first argue that since the 1980s, the roots of the equity bull market have been based upon a combination of factors, some political and some structural, which are now in the process of reversing. This shift will create serious headwinds to equities and poses a significant challenge to the dominance of passive strategies.

“It’s the Economy, Stupid”

Charles de Gaulle is reported to have said, “How can you govern a country which has 246 varieties of cheese?” and in that context, recent French civil disobedience is hardly unusual. When you factor in recent events in the UK, Italy or the US, it’s hard not to notice common themes. There is clearly an economic component. “Gilet Jaune” demands have included the reintroduction of the “solidarity tax” on wealth, lower fuel taxes and a minimum wage increase. This chimes with many of the demands of Italy’s 5 Star (M5S) and its broad pushback against Eurozone austerity, which has dogged growth since the GFC. In the US, there’s no question that the fading American Dream for large sections of voters played an important role in Trump’s election.

But What Do They Want?

However, if it were just the economy, it would suggest a relatively clear policy response. Unfortunately, as the French philosopher, Bruno Latour noted on French radio; “we have the yellow vests who don’t know exactly what they want and a government that’s completely incapable of listening”. Latour’s observation applies just as well to the UK. Many of those who voted for Brexit appear to have seen this as an opportunity to vote against a status quo which has slowly but relentlessly reduced their standard of living, without having any firm idea of what should replace it. Vague questions of national identity coalesced around unhappiness with the economic status quo and distrust of a European superstate. In the case of Brexit, this enabled UKIP (a populist anti-immigration party) to sweep up everyone from Conservative old ladies to disaffected Labour supporters. In the US, Trump’s nationalist politics appealed to everyone from union workers to the hard right. In a sense, what we are seeing is a serious challenge to the status quo of globalisation, and the free movement of labour, production and capital without really having any firm idea of what should replace it.

Understandably, the effect on traditional political parties has been corrosive. In the UK, both parties are chronically divided as they struggle to find a Brexit position which doesn’t inflict economic calamity or destroy what little party cohesion remains. In Italy, the populist coalition has ended the cosy (if fractious) post-war consensus politics, only to run straight into a showdown with the EU.

Who opened that Overton Window?

Here in the US, Trump’s election has so polarised politics that government shut down for a record period over the proposed border wall. In France, Macron has cleverly bought himself time with his “grand débat” gambit, a sort of “we are listening” tour. Whether it does more than paper over cracks is yet to be seen. Historically, it is in environments like this that radicals come to power. A few years ago, it would have been unthinkable that the country that gave the world Thatcherism could ever elect a party that advocated mass re-nationalisation of industry. Some recent opinion polls show Corbyn’s Labour is now neck and neck with the Tories. While we at MI2 hope that never happens, it is inescapable that the “Overton Window” (defined as the window of permissible political discourse) is widening. Policy alternatives which not that long ago would have been written off as “kooky” are now being openly aired. In this respect, the rise to prominence of Alexandria Occasio-Cortez is significant, not just because she is calling for a top tax rate of 70% but because she is a representative of the new generation that will eventually take over Congress.

Why have Equities Performed so well Since the ‘80s?

To some extent, these developments are unsurprising as part of the cycle of history. However, that is all the more reason that they cannot be ignored. Let’s not forget that a large part of the performance of risk assets over the last 40 years is a result of a similar political backlash against the ‘70s. Very simply, by the time Reagan and Thatcher came along, electorates were so sick of the excessive power of organised labour, and the associated inflation, that they were willing to vote for systematic and wide-ranging reform. We entered a halcyon period for markets with the policy emphasis on free markets, deregulation, and reduced taxation. These three factors combined with structural changes in demographics, globalisation and technology, have boosted corporate profits, driven down bond yields and enabled growing leverage and higher asset prices since the end of the ‘70s.

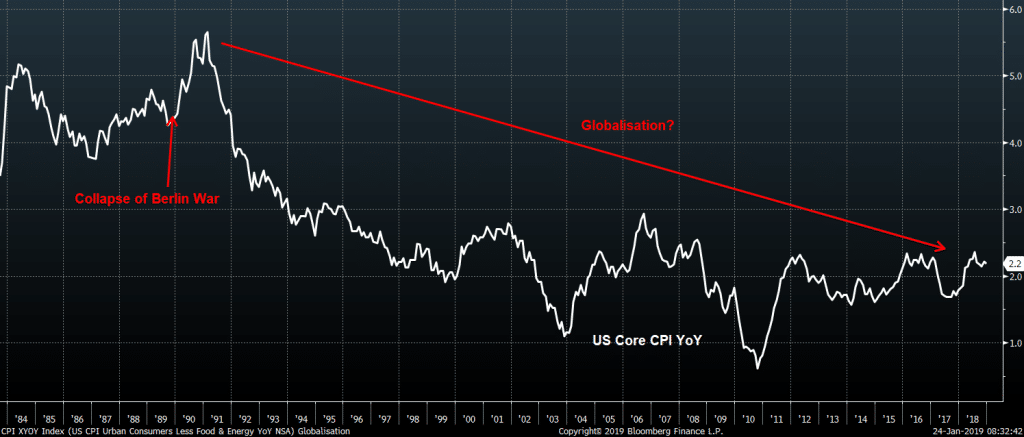

Globalisation

The end of the Cold-War and the collapse of the Berlin Wall in 1989 ushered in a new age of Globalisation-driven disinflation. China’s reintegration into the global economy has been the key to this, allowing global corporations access to the vast reserves of Chinese workers as Chinese peasants moved from the rural areas to the urban coast. This movement was essential for China’s economic development, but it was also an amazing opportunity for US and European corporations to arbitrage global labour markets and potentially open vast new product markets. China’s trade policy, which allowed producers to effectively avoid paying Value Added Tax (VAT) for exports and the undervaluation of its currency since 2002, has resulted in an overdeveloped export sector and distortion of its overall economy. The global macro effects have been profound; suppressing global inflation, while also creating huge financial imbalances which have helped further drive down bond yields and thereby encourage and enable leverage.

Technology/Productivity Growth

Advances in technology, particularly information technology, communications and logistics have facilitated extended, more complex, and vastly cheaper supply chains. These advances also allowed corporations to return equity, further boosting returns. The process is fascinating because, in its ultimate form, companies become creatures of pure IP. No longer forced to get dirty figuring out production engineering challenges, they have focused on design, innovation and marketing, all the time shedding expensive staff and economising on deployed capital while still increasing profits. Production facilities were either kept in-company but moved to lower cost locations like China or Mexico, or they were outsourced completely.

Demographics

Demographics, and particularly the trend towards increased longevity, played a role as well. In the early ‘70s, most Western European workers would have expected their compensation to include a component of retirement income or pension. This meant that employers took on both investment risk and longevity risk. Both were dramatically underestimated. The implicit cost of pensions represented a timebomb on the balance sheet of corporations, and sensible politicians recognised the problem. Market-driven solutions which relied on the individual to assume the longevity and investment risk were devised; for example, the 401k in the US. However, the terms on which this shift took place was costly for workers, particularly in the light of the massive decline in discount rates over the period. Put another way, corporations dodged a bullet in not picking up more of the tab for increases in longevity. Demographics required a shift away from Pay-Go pension provision, which has boosted asset prices by widening the universe of buyers.

Less well understood is the impact demographics have had on political dynamics. Baby boomers have dominated our electorates and are only just starting to leave the population. Electorates vote with their self-interest in mind; older electorates vote for deflation, younger ones for inflation.

With these processes, it’s not hard to see why corporations have been big winners since 1980. The share of corporate profits as a percentage of GDP has risen to levels last seen at the end of the “Gilded Era”. Equity investors should be asking themselves whether this is sustainable?

So, Who Lost?

While global corporations, especially in the US and China have reaped substantial benefits, workers in the developed world have been left to deal with the adjustment costs. That’s especially the case in the US where they have they been forced to compete indirectly not only with cheap Chinese labour, but also immigration which meant they were competing directly with Latin American migrants. Since 1980, about 40mn immigrants have entered the US, 21mn of those from Latin America. Great for business, but less good for low-skilled wages.

Source: Economic Policy Institute

American workers that kept their jobs have seen their compensation, retirement provision and healthcare suppressed by Chinese disinflation. This is not to suggest there was any real choice. China would have industrialised, but the consequences are now just beginning to be understood. Making matters worse, by actively embracing China at the same time labour markets were being deregulated, the speed of adjustment required was brutal, as was the decline in US pay and conditions for those exposed to the competition. The result has been unprecedented wealth transfer, a de-legitimisation of the political establishment and Steve Bannon’s “deplorables” delivering one of the biggest election upsets to the global liberal elite in US history.

Conditions for Less-Educated Americans are Dire

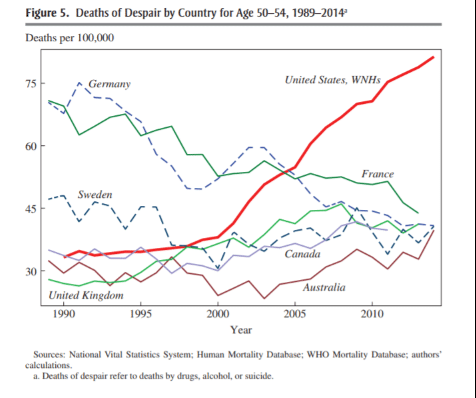

There is increasing evidence that the welfare position of the lower income groups in the US is stressed. Stressed enough to generate populist political pushback. To quote Angus Deaton, a Professor of Economics at Princeton, “There really has been a decline of the American working class. They reached their heyday with the blue-collar aristocracy with good union jobs and regular promotion and built a middle-class life. It has become harder and harder to replicate this.” The declining share of wages in GDP alone is not proof that the US working and middle classes are stressed enough to push back politically, but as we discussed above, there is evidence that they are pushing back. In “Mortality and Morbidity in the 21st Century,” Princeton Professors Anne Case and Angus Deaton followed up on their 2015 paper that revealed a shocking increase in midlife mortality among white non-Hispanic Americans, exploring patterns and contributing factors to the troubling trend.

Source: Case Deaton, “Morbidity and Mortality Trends in the US”

Case and Deaton find that while midlife mortality rates continue to fall among all education classes in most of the rich world, middle-aged, non-Hispanic whites in the U.S. with a high school diploma or less have experienced increasing midlife mortality since the late 1990s. This is due to both rises in the number of “deaths of despair”—death by drugs, alcohol and suicide—and a slowdown in progress against mortality from heart disease and cancer, the two largest killers in middle age.

The trends in other English-speaking countries provide something of a warning flag; Australia, Canada, Ireland, and the United Kingdom stand out among the comparison countries in having substantial trend increases in mortality from drugs, alcohol, and suicide during this period. However, their increases are dwarfed by the increase among U.S. non-graduate whites. Case-Deaton argue that stagnant incomes on their own do not explain the higher mortality rates. Instead, they propose a theory in which cumulative disadvantage from one birth cohort to the next is triggered by progressively worsening labour market opportunities at the time of entry for whites with low levels of education. This story, which fits the data, has the profoundly negative implication that the trend is likely to worsen regardless of any steps taken now. Case has suggested that physical and mental distress may bolster candidates like Donald Trump and Bernie Sanders. And while it’s only suggestive, the Washington Post and a Gallup Poll showed strong correlation between support for Trump and higher death rates. It stands to reason that those with little stake in the system are the least invested in preserving it.

The Middle Class are Not Much Better Off

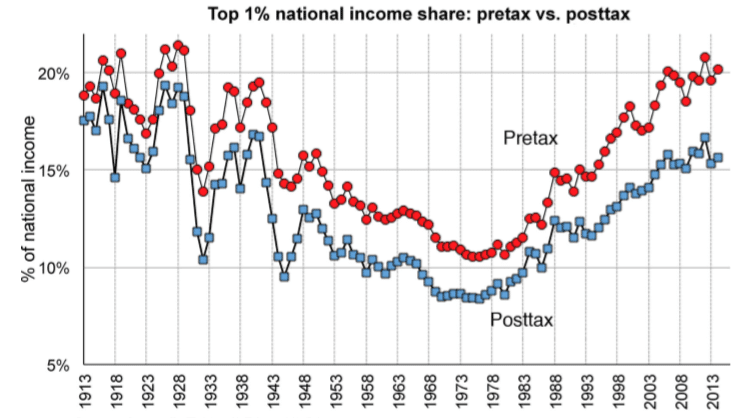

Once upon a time being middle class was a mark of independence and respectability. But no longer. As Jeffrey Pfeffer, Professor of Organizational Behaviour at the Stanford Business School notes the share of means-tested transfers, i.e. government benefits going to the “middle class” (the middle 60% of the income distribution) has more than doubled since 1979, to match the level of spending on families in the bottom fifth, according to Current Population Survey (CPS) data analysed by the Congressional Budget Office (CBO). And income distribution trends provide further evidence of slippage in the middle-class position. The Piketty-Saez paper made a splash when it came out, probably because it told people something they already suspected, rather than because it was a surprise. Once again, it is striking that pre-tax incomes for the top 1% have reached levels last seen in 1929.

Conclusion

In Part 1, we have argued that the strong (exceptional in the case of the US) equity market performance since the 1980s reflects the interaction of favourable trends in demographics, globalisation, and technology with the ‘80s policy shift towards “laissez-faire” free markets. This combination has increased corporate profitability and boosted asset valuations while reducing the share of GDP going to labour. This is why we have seen an increase in income inequality and wealth transfers on a scale last seen at the end of the “Gilded Age”. We suggest that the “Crisis of Populism” we are now seeing in the US, France, Italy and UK are directly related to these trends.

In Part 2, we will continue with how the laissez-faire policies of the 1980s have conditioned competition policy (anti-trust) and helped US margins expand toward the highs of the last 50 years. The shifts in favour of corporations have contributed towards divergence in generational interests just as we are fast approaching the point where we should expect a generational transition of political power. Millennials are reaching an age where we can expect them to be increasingly politically active. We discuss the Straus and Howe’s theories of Generational cycles, their predictions and the increasing evidence that we have reached the point of political push back. As the baby-boomers retire, and millennials take over, we will face constant pressure to overturn the Reagan-Thatcher policy consensus as new politicians ride increasing voter dissatisfaction. We at MI2 expect to see increasing support for policies aimed at pushing wages higher, increasing competition or new benefits such as “Medicare4all”. The tailwinds that have supported profits and valuations for 35 years will turn into headwinds. Finally, we analyse what a reversion to mean for corporate margins and profitability might mean for stock prices, sector performance and valuations.