Summary

- Since the 80’s policy/political trends have all been supportive of corporate capitalism

- But Millennials are about to become the dominant voters and will pull support

- Mainstream politics is always slow to react, but both the left and right are changing tack

- This will impact tech, anti-trust laws, pharma, buybacks, taxes and fiscal spending

The blood-dimmed tide is loosed, and everywhere

The ceremony of innocence is drowned;

The best lack all conviction, while the worst

Are full of passionate intensity.

-WB Yeats

In RIP Corporate Capitalism: Part I (7th Feb), we analysed how exceptional equity performance since the 1980’s was driven by a combination of globalisation, demographics, technology and pro-market reforms; factors which improved productivity while suppressing costs and inflation. That trifecta delivered almost unprecedented corporate margin growth and, when combined with lower discount factors, rewarded firms for pursuing breakneck growth or leveraging their balance sheets. History tends to have a natural cycle, and when we examine the elements of what has been a virtuous cocktail for corporate capitalism, it’s not hard to see how the best days are behind us. In this piece, Part II, we focus on the areas of risk and their potential implications.

Demographics and Fading Collective Memories

Much of what we discussed in Part I focused on how baby boomers, sickened by the inflationary experience of the 70’s, voted for change in the form of Thatcher and Reagan. Fast forward to today, and we have a new Zeitgeist. People are sick of the inequality that they attribute to that very same unfettered capitalist impulse from the Reagan/Thatcher era. Millennials have inherited the mess and have little to no skin in the capitalist game. They perceive change for change sake as a realistic option and are about to displace Boomers as the largest generational cohort at the ballot box.

This idea that, as generations wax and wane, the lessons of the past are forgotten is one with which we have a lot of sympathy. Interestingly, not only does it gel with the work of Strauss and Howe’s The Fourth Turning but also with some of the patterns that underpin the Kondratieff cycle. Indeed, both theories are consistent with each other in regard to the current political and economic conditions. Strauss and Howe would describe the current situation as a “Fourth Turning”, and Kondratieff theorists might describe the present as the “Winter” phase. In both theories, these terms describe a period of acute economic weakness, institutional destruction and political turmoil, which frequently culminates in revolution or even war. While this stage is not entirely played out under either theory, we are nevertheless rapidly approaching another turn. A period when a new generation enters politics and is marked by renewed belief in strong institutions, i.e. government, less individualism, a sense of shared social direction, fairness, civic engagement and, crucially from a market point of view, renewed inflation.

Political Change

Of course, both frameworks are essentially unverifiable and can be dismissed as “mumbo-jumbo”. However, it is when you look at recent changes already shaping politics things get interesting. By way of example, let’s look at the policies proposed by Alexandria Ocasio-Cortes (AOC) vs a moderate Democrat and potential presidential candidate Joe Biden. Both are on paper in the same party, but otherwise, they have little in common and represent very different political views.

Biden is a successful businessman and centrist in the classic sense of the Clintons or Tony Blair, i.e. a champagne socialist. He represents the socially liberal and fiscally conservative baby boomers who support marginally higher taxes and spending. But only if it doesn’t adversely impact them or destabilise a system in which they still believe.

The constituency that supports AOC, on the other hand, couldn’t be more different. Like her, they have no skin in the game (her net worth is essentially zero). In fact, many are starting with negative equity thanks to crushing student loans. This burden due to legal changes pushed through by the Bush admiration is practically impossible to discharge via bankruptcy. In a world of sky-high house prices and capped income, there’s very little chance they will get on the property ladder. Finally, if that wasn’t enough, they are facing the issue of dealing with retiring Baby Boomers who will put the social security system under enormous pressure. Is it surprising this cohort is supportive of the policies of AOC or Bernie Sanders? This pattern is also visible in the UK, where young voters 18-24 are the pillar underpinning a radicalised Corbyn Labour Party.

Furthermore, it isn’t just the radical left-wing or populist right that are calling time. Even the American right is starting to notice the shifting sands. Tucker Carlson, a darling of the conservative right, aired a monologue on Fox in January that was, in essence, an indictment of current American capitalism. The diatribe excoriated the damage done by private equity with the support of “Too Big to Fail” banks. Carlson noted that “what you are watching is whole populations revolting against leaders who refuse to improve their lives”. He specifically highlighted the issue of opiate use and rising suicide rates, which we discussed in Part I. Significantly, while the segment sparked enormous controversy, the reaction was by no means all negative even in Conservative circles. Most of all, the segment underscored something we already knew, i.e. populism is on the rise in both parties, and market capitalism is not popular. Carlson: “If you care about America, you ought to oppose the exploitation of Americans, whether it is happening in the inner city or on Wall Street”.

Policy Consequences

It is easy to dismiss these policies as extreme. But with debate raging in all corners of the political spectrum on the sustainability of the current system with its huge inequality, the prospects for the status quo surviving unmolested seem vanishingly small. After all, while mainstream politicians are always fighting the last war, it’s only a matter of time before pandering to the electorate becomes a short-cut to election success. Markets should be braced not only for legislation but also the shifting of broad political discourse to areas that are critical to the existing structure of corporate capitalism.

National Security and the “Silicon Curtain”

At the end of last summer, we sent you a big picture geo-political piece outlining how Trump’s populist victory had brought the notion of “Chimerica” into question. Assimilating China into the global economy had been the basis of the US-Sino relationships for the last 20 years. That changed, and Trump’s China policy crossed the Rubicon (“US-China: When Love Breaks Down” 3rd September). At the time we wrote:

“Since the collapse of the Iron Curtain, we’ve accepted that free markets are the norm. But the reality is that’s only been the case for the last 30 years. Prior to 1989 and the fall of the Berlin Wall, there was no global marketplace. Instead, we traded with our friends, where the deciding factor wasn’t profits but the dictates of geopolitics and national interest.”

We stick by those words. As we’ve discussed on numerous occasions since, a trade deal is a given. But for all the spin that will accompany its passage, a full rapprochement of the US-Sino relationship is delusional. Very simply, the forces against a return to business as usual are too powerful. At the core is the populist agenda that excessive, unfair globalisation has hollowed out the US economy and undermined the middle-class standard of living. This assertion is now accepted across all political parties and is a perfect illustration of how the Overton Window, which we discussed in Part I, has shifted. But more importantly, this populist narrative has now been seized upon by a national security establishment that for years has been increasingly worried by the threat posed by China.

Their agenda includes ensuring that the US military can guarantee the security of its logistical supply chain in the event of a deterioration of relations with China. A recent report found nearly 300 areas where there was vulnerability. The agenda also incorporates blunting China’s ability to access Western technology more generally. As a result, the US and its allies (with minimal US pressure) are attempting to diversify their supply chains away from China. This is yielding dividends, most publicly regarding Chinese involvement in the build-out of 5G networks. But this is just the beginning. As we explained in September, US authorities have new powerful legislative tools via FIRRMA and the ECA 2018 Act, which will increasingly start to impact all areas of the US/Chinese technology relationship as the various bodies involved are staffed. We do not believe it is an exaggeration when some commentators talk of a new “Silicon Curtain” descending on the global economy. For markets, this represents both a structural loss of opportunity/revenue and an increase in costs, which has not been priced in.

The Competitive Environment

Another area where we believe US corporations are vulnerable is anti-trust. In the 19th Century, the US competitive environment was highly concentrated. Then came the Sherman Act of 1890 and the Clayman Act of 1914, which handed powerful anti-trust tools to populist Presidents like Roosevelt, Taft and (early in his term) Reagan, who broke up AT&T.

The AT&T break-up catalysed US companies to push back. Aided by a sympathetic William Baxter, Reagan’s Antitrust Chief, they argued that the US needed national champions to protect it from unfair competition (at the time, especially Japanese). So, while AT&T was broken up, follow-up action against IBM was dropped. Over time, relentless lobbying and increasingly sympathetic courts also shifted their interpretation of the law resulting in much higher levels of industrial concentration, which has reduced competition.

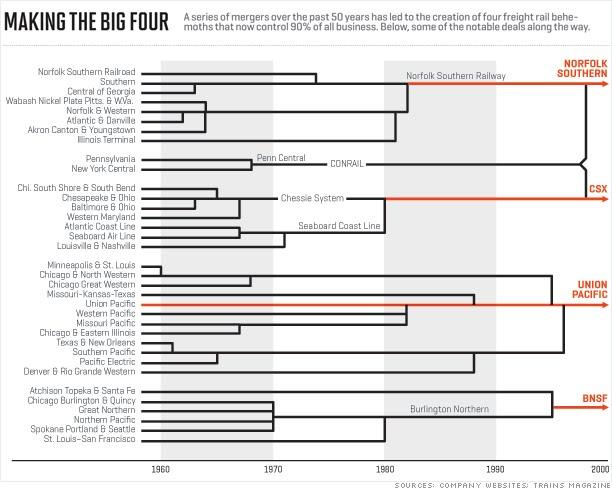

It is therefore unsurprising that we have oligopolistic markets across a swathe of US industries from beer, airlines, rail (below), potato chips to banking. What’s more, while many commentators point to the emergence of so-called “disruptors” as a sign that US competition is thriving, the reality is that in some cases these new entrants have been so effective that they now dominate even more comprehensively than the companies they displaced. Take Google and Facebook’s control of 80% of online advertising or the way Amazon has come to dominate retail. This increased concentration has resulted in excellent businesses to invest in, with fat margins, pricing power and the political heft enabling them to shape the regulatory environment in their favour.

However, there are signs that for all their lobbying firepower, the political tide is turning against companies. In terms of US antitrust policy, we already see increasing evidence of political pushback. Jonathon Tepper’s “The Myth of Capitalism” and Tim Wu’s “The Curse of Bigness” are both persuasive long-form examinations of how excess concentration is harming the US. The proposed T-Mobile/Sprint deal will be an interesting test of where enforcement is heading and recent comments from House Judiciary antitrust Chairman, David Cicilline, suggest broad scepticism about the deal. Cicilline also suggested that future tech hearings will touch on everything from data privacy to antitrust statutes and he was clear he expected FAANG CEOs to participate in the hearings. While we don’t think Amy Klobuchar is likely to be successful in the 2020 presidential race, she has made oversight of big tech and anti-trust her banner issues. Indeed, the timing couldn’t be worse for these firms because they are already struggling from Europe’s GDPR and the risk is that, as the debate picks up here in the US, this toxic piece of legislation becomes the global benchmark for data privacy.

Pharma – the drugs might work, but the prices don’t!

That brings us to pharma, where the building political backlash is likely so severe that it deserves a special mention. The biggest issue is unquestionably rising costs. A study by the US Government Accountability Office into the Drug industry in 2017 suggests the sector has done well to avoid Congressional cross-hairs. Prescription drug expenses have risen to about 12% of total personal healthcare spending, up from 7% in the 1990s. If companies are to be believed much of this is justified by the expense of bringing new drugs to market. But that doesn’t sit well with consumers and regulators. The profit margins of the top 25 drug companies averaged between 15% to 20% from 2006 to 2015 vs between 4% and 9% for other industries. During the same period, estimated biotech and pharma sales revenue rose from $534bn to $775bn as R&D spending increased 8%.

To make matters worse, high pharma margins are increasingly visible thanks to the internet. Cost-conscious diabetics are questioning why they should be paying so much for insulin vs their peers in Mexico or Canada. Mylan recently settled with the DoJ for $465mio as they failed to justify why an EpiPen cost $609 in the US while only costing the UK NHS $62?

So far, outside rare prosecutions, the impact on the sector has been minimal. That seems unlikely to last as it’s increasingly seen as a winning political issue. Chuck Grassley, the new chair of the Senate Finance Committee, is pushing legislation that is widely opposed by the industry. This would allow generic drugs to take a greater share of the market while allowing Americans to import cheaper drugs from Canada. Meanwhile, the Dems are throwing their support behind Trump’s proposals that Medicare would base drug payments for certain drugs on the prices that European countries pay.

Bottom line, while the most extreme proposals are likely to be lobbied away, pharma is fighting against the tide. With overall healthcare spending pushing towards 20% of GDP, and Millennials facing up to the costs of caring for their parents, change is inevitable. We expect to see more pressure for AOC’s proposed national health system and a single purchasing body to negotiate drug prices.

Share Buybacks

Buybacks have been a mainstay of the recent bull market and are viewed by many practitioners as a most effective tool, part of the inalienable right of a CEO to best manage the resources of their firm. Yet, a disproportionate share of the benefits from share buybacks accrue to corporate executives and the 1%. To make matters worse, as we have seen with GE, it is increasingly apparent that, far from strengthening a firm’s prospects, the debt that frequently accompanies these programmes has imperilled company’s long-term survival. In the current politically-charged environment, enabling the select few to make out like bandits or, to use the historical analogy, robber barons, while potentially endangering US jobs (and communities that these firms support) isn’t just politically unjustifiable but morally wrong.

Both parties have now sponsored initiatives aimed at inhibiting stock buybacks. The Democratic Schumer-Sanders Bill requires companies to meet a laundry list of conditions (minimum wages, seven days paid sick leave, healthcare benefits, pensions, etc.) before permitting buybacks. The competing Republican Rubio Bill would raise the capital gains tax rate applied to buybacks. Neither strike us as being well thought-out, and when it comes to optimal corporate capital structure, we aren’t convinced that Congress has the answers. However, even if neither of these bills see the light of day, they highlight a very striking political change. It isn’t hard to imagine a time in the future where buybacks become un-PC and, like offshoring or buying Chinese tech products, un-American.

Workers Share of the Pie

In the same vein as Buybacks, wages are an issue that focuses the political spotlight on inequality. This is hot topic for Millennials who lack wealth and so need rapid wage growth to ever have any hope of matching their parents’ lifestyle. AOC’s support for a national minimum wage speaks to this issue. But right across the globe, wages have become a contentious issue and have elicited numerous policy responses.

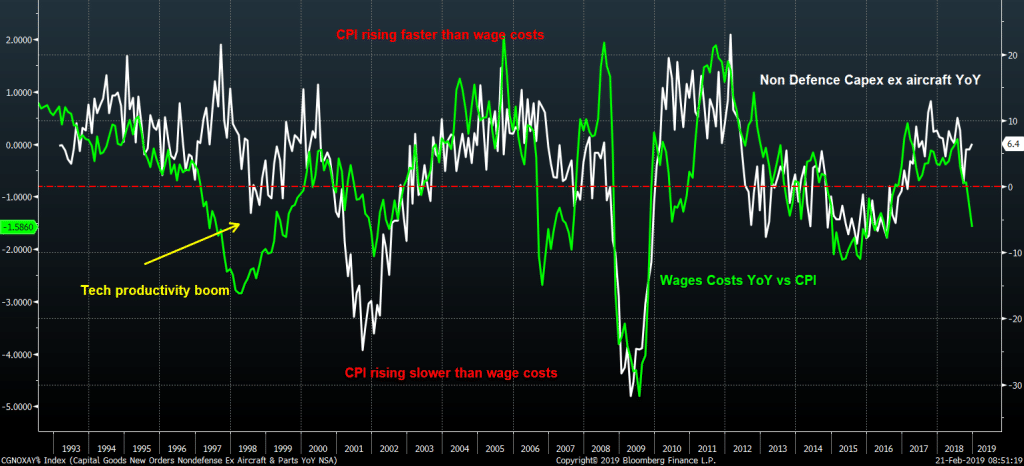

Interestingly, it isn’t just the politicians. What has recently piqued our interest is the way the Fed appears to be de-emphasising the inflationary risks of an overheating labour market. Perhaps, they have all finally drunk the cool-aid that the Phillips curve is dead. But it does suggest they are more than willing to support much higher wage growth. We believe that, provided we don’t end up in a recession, wages are set to move higher after a pause. (Our base case is the Fed is moving to prevent any risk of recession). However, what equity investors don’t appreciate is that this is potentially horrible for corporate margins, which lag wages by two years and have only recently diverged thanks to the Trump tax cuts.

Furthermore, we think it’s unlikely that we get a repeat of the late 1990’s, capex induced productivity boom, which allowed both margin and wages growth. For capex, firms need positive cash flow, and if we model that using CPI vs Average Earnings, it’s dropping sharply.

MMT, Taxation and Inflation

As we’ve discussed, Millennials rightly feel they’ve been dealt a rough hand. Unsurprisingly, and right on cue for S&H’s next “Turn”, the dominant demographic cohort will be pushing a political agenda that emphasises fairness, inclusion, stability, civic duty and greater government involvement. This will include higher wages, healthcare and childcare alongside things like plans to cut carbon emissions (don’t forget this generation scooters to work). None of this will come cheap.

There seem to be two schools of thoughts on how to pay for it. Taxation is the obvious choice. AOC’s call for a 70% on the ultra-rich is totemic. Michael Dell’s outright dismissal of the idea at Davos smacks of paying the high! However, as tax experts will tell you, taxing the wealthy is notoriously hard because capital is mobile. That doesn’t mean the left won’t try. Elizabeth Warren’s proposal for a 2% wealth tax on family assets over $50mio gets interesting because, at the end of the day, an asset is an asset whether it is domiciled in New York, Florida or Delaware. Furthermore, if taxes are skewed towards property, even wealthy Italians who loathe their “Immobiliare” tax will confirm it is hard to avoid. It would also have the benefit of catching all those “non-domicile” residents, be they a CT-based hedge fund manager with a $100mio NYC apartment or a Saudi Prince with a London pied-a-terre. All of this plays well to the idea of correcting wealth disparities.

The other potential route is a massive expansion of the fiscal deficit. In this respect, the steady increase in traction of Modern Monetary Theory (MMT) on the left is striking. MMT postulates that if a country has its own sovereign currency, there can never be a real deficit constraint because government spending definitionally generates sufficient funds in the banking system to fund the spending. It’s not so much a theory but rather an accounting identity. The constraint is not financial but resource-driven. So, absent accelerating inflation, there is no good reason not to expand deficits further. To macro-wonks like ourselves, the thesis is fascinating and just another example of generational cycles: The young rediscovering an approach that was discredited in the 70s. The approach is gaining traction as a Millennial restatement of 60’s Keynesian orthodoxy. If MMT does become the new orthodoxy, it will serve as the intellectual rationale for a shift in policy bias from deflation to inflation just as the Millennials become the largest generational group. Funny how that happens!

Conclusion

There is a natural cycle to history. Whether it is a function of simple demographics or the more complex formulations suggested by Kondratieff or S&H is perhaps academic. What we do know is that at the turn, by definition, existing trends are pushed to extremes. Thus far, mainstream politics (which is always reactive) is just sensing that the tide is turning. But when it does, its legislative engagement solidifies and amplifies the direction change and, in the same way a joke ten years ago that would have elicited a peal of laughter is now utterly un-pc, it changes behavioural norms.

At MI2 we aren’t concerned with social justice; we are only focused on markets. But in that context, the political environment is part of our trading environment, and current trends aren’t sustainable. That means that as older richer baby boomers are replaced by young, indebted Millennials as the dominant electorate, self-interest will dictate that the agenda switches. Hence, deregulation, individualism and disinflation are out, and bigger government, collectivism and inflation are in. It may take a decade for us to get there. But we would caution against being too dismissive because, at a turn, even a modest shift in the wind can feel like a tempest.

For markets, and especially equities, the implications are profound. In the US, profits as a share of GDP are currently over 5%, i.e. well over double the norm from the end of WWII to the mid-1980s. Even a slight correction would be enormously destructive to valuations but would go a long way to resetting current intergenerational wealth disparities. Alternatively, and much more palatably, if Millennials get the inflation they need, then we can get the correction via stagnating profits as wage earners take the lion’s share of any growth in the cake.

Ultimately, it’s very difficult to make sensible forecasts on this scale. However, if forced to choose between arguing for further increases in profits as a share of GDP or a mean reversion in conditions, we would go for the latter. The last 40 years have served up the perfect cocktail for corporate capitalism. That party is coming to an end.